Become an expert and watch your personal growth soar to new heights!

GAAP vs IFRS? #

GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards) are two prominent sets of accounting standards that guide how companies prepare and present their financial statements.

GAAP (Generally Accepted Accounting Principles):

- Origin: Developed and maintained by the Financial Accounting Standards Board (FASB) in the United States.

- Scope: Primarily used by companies based in the United States and those that list their securities on U.S. stock exchanges.

- Focus: GAAP is more rules-based, providing specific guidelines and procedures for various accounting transactions and situations.

- Strengths:

- Well-established and understood within the U.S. business community.

- Provides detailed guidance, leaving less room for interpretation.

- Strong emphasis on industry-specific guidance.

- Weaknesses:

- Can be complex and rigid, potentially hindering flexibility.

- May not always align with international accounting practices.

- Less adaptable to changes in the global business environment.

IFRS (International Financial Reporting Standards):

- Origin: Developed and maintained by the International Accounting Standards Board (IASB).

Scope: Used by companies in over 140 countries worldwide, including most of Europe, Asia, and South America. - Focus: IFRS is more principles-based, providing broader guidelines and requiring more judgment from accountants.

- Strengths:

- Promotes comparability and consistency of financial statements across countries.

- More flexible and adaptable to changes in the global business environment.

- Simplifies consolidation for multinational companies.

- Weaknesses:

- Can be less specific than GAAP, leading to potential inconsistencies in interpretation.

- May require additional training for accountants who are accustomed to GAAP.

- Less industry-specific guidance compared to GAAP.

Key Differences:

| Feature | GAAP | IFRS |

|---|---|---|

| Basis | Rules-based | Principles-based |

| Inventory Costing | LIFO (Last-In, First-Out) allowed | LIFO prohibited |

| Development Costs | Generally expensed | Can be capitalized under certain conditions |

| Intangible Assets | Stricter criteria for recognition | More lenient criteria for recognition |

| Revaluation of Property | Not allowed | Allowed under certain conditions |

Convergence Efforts:

Efforts have been made to converge GAAP and IFRS to create a single set of global accounting standards. While progress has been made, complete convergence remains a long-term goal.

GAAP and IFRS are like two different sets of rules for keeping score in a game.

GAAP vs IFRS SUMMARY

GAAP (Generally Accepted Accounting Principles):

- The rulebook used in the United States.

- Very detailed and specific, like a referee’s handbook.

- Leaves little room for interpretation, so everyone plays by the same exact rules.

IFRS (International Financial Reporting Standards):

- The rulebook used in most other countries.

- More flexible, like a coach’s playbook.

- Gives general guidelines, but allows for some interpretation and adaptation to different situations.

Why it Matters:

Just like different sports have different rules, companies in different countries may use different accounting standards. This can make it tricky to compare financial results across borders. However, both GAAP and IFRS aim to provide a fair and accurate picture of a company’s financial performance, ensuring transparency and trust for investors and stakeholders.

Key Principals of IFRS #

Key principles of IFRS that are essential to understand:

- Accrual Accounting: IFRS mandates the use of accrual accounting, meaning transactions are recorded when they occur, not just when cash changes hands. This provides a more accurate picture of a company’s financial position and performance.

- Fair Value Measurement: IFRS emphasizes fair value measurement for certain assets and liabilities. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

- Going Concern: IFRS assumes that a company will continue to operate in the foreseeable future. This assumption allows for the use of accrual accounting and historical cost measurement.

- Substance Over Form: IFRS requires transactions and events to be accounted for in accordance with their economic substance rather than their legal form. This means looking beyond the legal structure of a transaction to understand its economic impact.

- Relevance and Faithful Representation: Financial information should be relevant to the users’ decision-making needs and faithfully represent the economic phenomena it purports to represent. This means it should be complete, neutral, and free from error.

- Comparability: Financial statements should be prepared in a way that allows for comparison over time and with other entities. This means using consistent accounting policies and providing sufficient disclosures.

- Understandability: Financial statements should be presented in a clear and concise manner that is understandable to users with a reasonable knowledge of business and economic activities.

- Timeliness: Financial information should be made available to users in time to be capable of influencing their decisions.

- Materiality: Information is material if omitting, misstating, or obscuring it could reasonably be expected to influence the decisions of users of the financial statements.

- Consistency: A company should apply the same accounting policies from one period to the next unless a change is required by IFRS or would result in a more reliable and relevant presentation of the financial statements.

By adhering to these principles, bookkeepers can ensure that financial statements prepared under IFRS are transparent, reliable, and comparable, providing useful information to investors, creditors, and other stakeholders.

What is Cost of Goods Sold (COGS)? #

Cost of Goods Sold (COGS) aka Cost of Sales (COS) is a crucial accounting term that represents the direct costs incurred in producing the goods or services a company sells. It’s a key figure on a company’s income statement and provides valuable insights into its profitability and efficiency.

For manufacturers or retailers of physical products, COGS typically includes:

- Direct Materials: The raw materials and components used to create the product.

- Direct Labor: The wages and benefits paid to workers directly involved in manufacturing or assembling the product.

- Manufacturing Overhead: Indirect costs associated with production, such as factory rent, utilities, depreciation of manufacturing equipment, and the salaries of production supervisors.

For service-based businesses, COGS might include the direct costs of providing the service, such as:

- Labor Costs: Wages and benefits paid to employees who directly deliver the service.

- Materials and Supplies: Costs of any materials or supplies used in providing the service.

What’s NOT Included in COGS:

COGS does not include indirect costs or operating expenses, such as:

- Selling, General, and Administrative (SG&A) Expenses: Costs related to marketing, sales, distribution, and general administration.

- Research and Development (R&D) Costs: Expenses incurred in developing new products or services.

How COGS is Calculated:

The basic formula for calculating COGS is:

Beginning Inventory + Purchases – Ending Inventory = Cost of Goods Sold

This formula accounts for the cost of goods that were available for sale during a period, subtracts the cost of goods that remain unsold (ending inventory), and the result is the cost of the goods that were actually sold (COGS).

Why COGS is Important:

COGS is a key component in determining a company’s gross profit, which is calculated as:

Revenue – Cost of Goods Sold = Gross Profit

Gross profit is a critical measure of a company’s profitability, as it indicates how much money is left over from sales after accounting for the direct costs of producing the goods or services.

By analysing COGS, businesses can:

- Assess Profitability: Understand how much it costs to produce their products or services and identify opportunities for cost reduction.

- Price Products Competitively: Set prices that cover costs and generate a reasonable profit margin.

- Evaluate Inventory Management: Ensure that inventory levels are optimized to meet demand without tying up excessive capital.

- Compare Performance: Compare COGS over time or against industry benchmarks to assess operational efficiency.

Understanding COGS is crucial for business owners, managers, and investors, as it provides valuable insights into a company’s financial health and profitability.

Cost of Sale (COS) at Point of Sale #

Sometimes you will run into customers where the accountant wants to record COS at Point of Sale. Most of the time, the accountant for that customer would have worked for a company such an Original Equipment Manufacturer or “OEM”. With most manufacturing businesses, they use the accounting for COS at point of Sale. VMG’s accrual-based system DOES NOT.

It will help you to understand what it means to account for a COS at Point of Sale.

Cost of Sale for Manufacturers:

In manufacturing, the “cost of sale” (also known as “cost of goods sold” or COGS) refers to the direct costs associated with producing the goods that were sold during a specific period. This includes:

- Direct Materials: The raw materials used in production (e.g., steel for a car manufacturer, fabric for a clothing manufacturer).

- Direct Labor: The wages and benefits paid to workers directly involved in producing the goods (e.g., assembly line workers, machine operators).

- Manufacturing Overhead: Indirect costs associated with production, such as factory rent, utilities, and depreciation of manufacturing equipment.

Recording Cost of Sale at the Point of Realization (Accrual Accounting):

Manufacturers typically use accrual accounting, which means the cost of sale is recognized on the income statement only when the sale of the finished goods is realized. This is because:

- Matching Principle: Accrual accounting follows the matching principle, which requires expenses to be matched with the revenues they help generate. In the case of manufacturing, the cost of producing goods is matched with the revenue earned from selling those goods.

- Inventory Accounting: Until the goods are sold, they are considered assets (inventory) on the balance sheet. The cost of these goods is not expensed until they are sold and the revenue is recognized.

Illustrative Example:

Let’s say a car manufacturer produces 100 cars in a month, but only sells 80 of them.

- The cost of producing all 100 cars (direct materials, direct labour, and manufacturing overhead) is recorded in an inventory account on the balance sheet.

- When 80 cars are sold, the cost of producing those 80 cars is transferred from the inventory account to the cost of goods sold (COGS) account on the income statement.

- The remaining 20 cars and their associated production costs remain in the inventory account until they are sold in a future period.

Benefits of this Approach:

- Accurate Financial Reporting: By recognizing the cost of sale only when revenue is realized, accrual accounting provides a more accurate picture of a manufacturer’s profitability during a specific period.

- Inventory Management: This approach helps manufacturers track inventory levels and costs more effectively.

- Compliance with Accounting Standards: Recording cost of sale at the point of realization aligns with Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS).

VMG and Cost of Sales (COS) #

VMG’s Approach to Cost of Goods Sold (COGS): Prioritizing Real-Time Financial Accuracy

While traditional manufacturers record COS at the point of sale, VMG DMS Accounting adopts a different approach specifically tailored for dealerships. We record the cost of sales (COS) the moment your dealership receives an invoice from the supplier, even if the vehicle hasn’t been sold yet.

Why This Approach Makes Sense for Dealerships:

- Inventory is an Asset: Unlike manufacturers, dealerships primarily purchase finished goods (vehicles) that are ready for sale. These vehicles represent a significant investment and are considered assets on the dealership’s balance sheet.

- Accurately Reflecting Financial Position: By recording COS at the point of invoicing, VMG DMS Accounting provides a more accurate and up-to-date picture of the dealership’s financial position. This is crucial for making informed decisions about inventory management, pricing, and profitability.

- Streamlined Accounting: This method simplifies the accounting process by eliminating the need to track individual vehicle sales and match them with corresponding purchase invoices. It ensures that COS is consistently recorded and allocated across all inventory.

- Compliance and Transparency: Recording COS at invoicing ensures compliance with accounting standards and provides a transparent view of the dealership’s financial health to stakeholders, including investors and lenders.

Key Points :

- Dealerships are not manufacturers: Highlight the fundamental difference between dealerships (retailers of finished goods) and manufacturers (producers of goods).

- Inventory as an asset: Explain that vehicles in a dealership’s inventory are considered assets and their cost should be recognized as soon as they are acquired.

- Real-time financial accuracy: Emphasize that recording COS at invoicing provides a more accurate and timely view of the dealership’s financial performance.

- Simplified accounting: Highlight the streamlined accounting process and reduced administrative burden that comes with this approach (i.e: reduced Journals).

What is the Difference Between an Expense and Cost of Sale? #

For a used car dealership that records Cost of Sale (COS) at the point of invoice, here’s how COS and Expenses differ:

SIMPLE ANSWER: COS affect GP and Expenses affect NP.

Cost of Sale (COGS):

- What it is: The direct cost of acquiring the vehicles you have in inventory, including:

- Purchase price: The amount paid to the previous owner, auction, or wholesaler.

- Auction fees: Any fees associated with purchasing the vehicle at auction.

- Transportation costs: Cost incurred to transport the vehicle to your dealership.

- Registration Costs (aka Dealer Stock): Occurs when registering ther vehicle into the Dealerships name.

- Licence and Registration Costs: Occur when the vehicle is registered out of the Dealerships name into their customers name.

- Reconditioning costs (at purchase): Initial repairs, detailing, or other work necessary to make the car sellable upon arrival.

- Reconditioning costs (post-purchase): Any additional repairs or improvements made to the vehicle while it’s in inventory.

- Accounting: COS is recognized and recorded the moment the invoice for the vehicle is received from the supplier, even before the car is sold.

- Key point: COS represents the value of the vehicle as it sits in your inventory, ready for sale.

Expenses:

- What they are: All other costs incurred to run your dealership, including:

- Salaries and wages: Payments to sales staff, administrative staff, mechanics, and lot attendants.

- Marketing and advertising: Costs of promoting your dealership and inventory.

- Rent and utilities: Costs for your dealership’s physical location.

- Insurance: Premiums for vehicle and liability insurance.

- Interest expense: Interest paid on loans used to finance inventory or operations.

- Depreciation: The decrease in value of assets like vehicles, equipment, and buildings over time.

- Other operating expenses: Office supplies, software subscriptions, legal fees, etc.

- Accounting: Expenses are recorded in the period they are incurred, regardless of when (or if) a vehicle is sold.

- Key point: Expenses represent the costs of running your business and are separate from the value of your inventory.

Why This Distinction Matters in VMG DMS:

- Inventory Valuation: Recording COS at the point of invoice provides a more accurate valuation of your inventory, as it reflects the actual cost of acquiring the vehicles.

- Profitability Analysis: By separating COS and expenses, you can clearly see how much profit is generated from the sale of vehicles.

- Financial Planning: Understanding your true cost of goods and operating expenses allows for better budgeting, pricing decisions, and overall financial management.

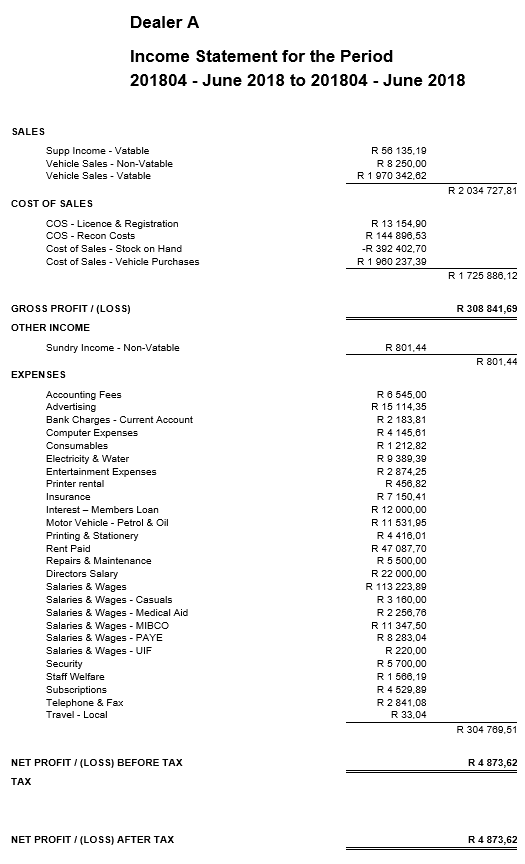

Understanding the Income Statement #

An income statement, also known as a profit and loss (P&L) statement, serves several crucial purposes for businesses:

- Measures Financial Performance: The primary function of an income statement is to show how much profit (or loss) a company generated during a specific period, usually a quarter or a year. It details the revenues earned and the expenses incurred, ultimately revealing the net income or bottom line.

- Assesses Profitability: By analysing the different components of the income statement, such as gross profit, operating profit, and net profit, businesses can evaluate their profitability. This helps them understand how effectively they are generating revenue and managing costs.

- Tracks Trends and Changes: Comparing income statements from different periods allows businesses to identify trends in their financial performance. Are revenues increasing? Are expenses growing faster than revenue? These insights are vital for making informed business decisions.

- Informs Decision-Making: The income statement is a key tool for management to make informed decisions about pricing, cost control, investments, and overall business strategy. It helps them understand where the company is making money and where it’s losing money, enabling them to take corrective action if needed.

- Attracts Investors and Lenders: Investors and lenders use income statements to assess a company’s financial health and profitability. A strong income statement can help a company attract investment capital or secure loans, while a weak one may raise concerns and make it difficult to raise funds.

- Evaluates Management Performance: The income statement can be used to evaluate the effectiveness of management’s decisions and strategies. Are they generating sufficient revenue? Are they controlling costs effectively? These insights can help stakeholders assess management’s performance and hold them accountable.

- Benchmarking: Comparing a company’s income statement to industry peers can help identify areas where the company is performing well or lagging. This information can be used to benchmark performance and set goals for improvement.

In summary, the income statement is a fundamental financial statement that provides a snapshot of a company’s profitability over a specific period. It’s a valuable tool for managers, investors, lenders, and other stakeholders to understand the company’s financial performance, make informed decisions, and plan for the future.

What is Meant by Above the Line and Below the Line? #

In accounting and finance, “above the line” and “below the line” refer to specific sections of a company’s income statement, with the “line” typically representing gross profit.

Above the Line:

- Location: This section appears above the gross profit line on the income statement.

- Items Included: Primarily includes revenues and the cost of goods sold (COGS) or cost of sales (COS). These are directly related to the company’s core operations and revenue generation.

- Significance: These items directly impact gross profit, a key indicator of a company’s profitability and efficiency in producing or delivering its products or services.

Below the Line:

- Location: This section appears below the gross profit line on the income statement.

- Items Included: Includes operating expenses (rent, salaries, marketing), interest expenses, and taxes. These are indirect costs not directly tied to production or service delivery.

- Significance: These items affect the company’s net income (the bottom line), representing the profit after all expenses have been deducted.

Key Differences:

| Feature | Above the Line | Below the Line |

|---|---|---|

| Items | Revenue, Cost of Goods Sold (COGS) or Cost of Sales (COS) | Operating expenses, Interest expenses, Taxes |

| Impact | Directly affects gross profit | Indirectly affects net income |

| Focus | Core operations and revenue generation | Supporting functions and financing costs |

| Volatility | Can fluctuate more in the short term (e.g., with sales changes) | Often more stable and predictable (e.g., rent) |

Importance in Analysis:

The distinction between above and below the line items helps analyze a company’s financial performance.

- A high gross profit (above the line) might be offset by high operating expenses (below the line), resulting in a lower net income.

- Analyzing both sections can reveal a company’s efficiency in generating revenue and managing costs.

Note:

The terms “above the line” and “below the line” can have slightly different meanings in other contexts, such as marketing and film production. In those fields, they often refer to different types of advertising or budgeting.

The Income Statement Equation #

The basic income statement equation is:

Revenue – Expenses = Net Income

This simple equation summarizes a company’s financial performance over a specific period. Let’s break down each component:

- Revenue: The total amount of money a company earns from its primary business activities, such as selling products or services.

- Expenses: The costs incurred by a company to operate and generate revenue, including cost of goods sold (COGS), operating expenses (rent, salaries, marketing), interest expenses, and taxes.

- Net Income: The profit a company makes after subtracting all expenses from revenue. A positive net income indicates a profit, while a negative net income indicates a loss.

There are two main types of income statements:

- Single-Step Income Statement: Uses the basic equation above to directly calculate net income.

- Multi-Step Income Statement: Provides a more detailed breakdown by calculating several intermediate profit figures before arriving at net income. The typical format is:

Income Statement:

Revenue (Sales)

– Cost of Goods Sold (COGS)

= Gross Profit

– Operating Expenses

= Operating Income

+/- Non-Operating Income/Expenses (e.g., gains/losses on investments)

= Income Before Taxes

– Income Taxes

= Net Income (Profit after Tax)

You will notice in the equation above that Dividends no longer form part of the income statement as far as IFRS is concerned. Rather these are moved to the Statement of Changes in Equity report (Formula below):

Retained Earnings (Beginning Balance)

+ Net Income (Profit after Tax)

– Dividends

= Retained Earnings (Ending Balance)

Both types of income statements provide valuable information about a company’s financial performance and profitability, but the multi-step statement offers a more comprehensive analysis of the different components that contribute to the bottom line.

Understanding Accounting Periods #

An accounting period is a specific timeframe used to track and report a company’s financial activity. While it often aligns with calendar months, it doesn’t have to.

- Financial Year Start: The starting month of your client’s financial year becomes the first accounting period (Period 1).

- Sequential Periods: Each subsequent month becomes the next accounting period in sequence (Period 2, Period 3, and so on).

- Financial Year End: The month before the financial year starts again becomes the last accounting period (Period 12 in a 12-month financial year).

Example:

If your client’s financial year begins in March, their accounting periods would look like this:

- Period 1: March

- Period 2: April

- Period 3: May

- …

- Period 12: February

Why This Matters for Your Clients:

Understanding accounting periods is crucial for your clients because:

- Accurate Reporting: It ensures that financial reports (like profit and loss statements) reflect the correct timeframe, allowing for meaningful analysis of performance.

- Tax Compliance: Accounting periods are often aligned with tax reporting requirements, making it easier for businesses to file taxes correctly.

- Financial Planning: Knowing which period a transaction falls into helps with budgeting, forecasting, and making informed financial decisions.

Key Points for Trainers:

- Flexibility: Emphasize that while VMG DMS can accommodate different financial year starts, it’s crucial to set this up correctly from the beginning to avoid confusion and errors in reporting.

- Communication: Make sure clients understand their chosen accounting period structure and how it impacts their financial reports.

- Support: Offer guidance and support to clients if they have any questions or need assistance setting up or adjusting their accounting periods within the VMG DMS.